All Categories

Featured

Table of Contents

Costs are usually reduced than entire life policies. With a degree term policy, you can pick your coverage quantity and the plan size. You're not secured right into a contract for the remainder of your life. Throughout your policy, you never have to bother with the costs or survivor benefit amounts changing.

And you can't cash out your policy during its term, so you won't get any economic take advantage of your previous insurance coverage. Just like other sorts of life insurance policy, the expense of a level term plan relies on your age, coverage demands, employment, way of living and wellness. Generally, you'll locate more inexpensive insurance coverage if you're more youthful, healthier and much less dangerous to insure.

Because level term costs remain the same for the period of insurance coverage, you'll recognize exactly just how much you'll pay each time. Level term coverage likewise has some adaptability, allowing you to personalize your policy with added functions.

You may have to fulfill certain conditions and certifications for your insurance provider to pass this cyclist. There also could be an age or time restriction on the insurance coverage.

30-year Level Term Life Insurance

The survivor benefit is generally smaller, and protection usually lasts up until your kid transforms 18 or 25. This biker may be an extra affordable way to help guarantee your youngsters are covered as bikers can often cover several dependents simultaneously. When your youngster ages out of this insurance coverage, it may be possible to convert the cyclist into a brand-new plan.

When comparing term versus long-term life insurance policy, it is very important to keep in mind there are a few various types. The most common kind of irreversible life insurance policy is whole life insurance policy, but it has some crucial distinctions compared to level term protection. Here's a basic summary of what to consider when comparing term vs.

Whole life insurance policy lasts permanently, while term protection lasts for a certain period. The premiums for term life insurance policy are usually less than whole life insurance coverage. With both, the costs remain the very same for the period of the plan. Whole life insurance coverage has a cash value component, where a part of the costs might grow tax-deferred for future needs.

Can I get Level Premium Term Life Insurance online?

Among the main features of level term protection is that your premiums and your fatality advantage don't change. With reducing term life insurance, your costs remain the exact same; nonetheless, the survivor benefit quantity gets smaller sized with time. You may have coverage that begins with a death benefit of $10,000, which could cover a mortgage, and after that each year, the fatality advantage will certainly lower by a collection amount or percentage.

Due to this, it's often an extra budget-friendly kind of level term protection., however it might not be enough life insurance coverage for your needs.

After choosing on a plan, finish the application. If you're approved, sign the paperwork and pay your first premium.

You may want to upgrade your beneficiary details if you've had any considerable life adjustments, such as a marital relationship, birth or separation. Life insurance policy can often really feel difficult.

What is the most popular Compare Level Term Life Insurance plan in 2024?

No, level term life insurance coverage doesn't have cash money worth. Some life insurance policy plans have a financial investment feature that allows you to construct money value in time. What is level term life insurance?. A part of your premium settlements is established aside and can gain passion gradually, which grows tax-deferred during the life of your protection

Nonetheless, these plans are frequently considerably more expensive than term protection. If you reach completion of your policy and are still alive, the protection finishes. Nevertheless, you have some choices if you still desire some life insurance policy protection. You can: If you're 65 and your coverage has actually run out, for instance, you may wish to get a new 10-year level term life insurance policy plan.

Tax Benefits Of Level Term Life Insurance

You might have the ability to convert your term coverage into a whole life plan that will last for the rest of your life. Several kinds of level term policies are convertible. That implies, at the end of your coverage, you can transform some or every one of your plan to whole life coverage.

Level term life insurance is a plan that lasts a set term typically in between 10 and thirty years and includes a degree death benefit and degree costs that remain the very same for the whole time the plan holds. This means you'll recognize precisely just how much your settlements are and when you'll have to make them, allowing you to spending plan appropriately.

Degree term can be a wonderful choice if you're wanting to purchase life insurance protection for the first time. According to LIMRA's 2023 Insurance Measure Research, 30% of all grownups in the U.S. need life insurance and don't have any type of kind of policy yet. Level term life is foreseeable and economical, that makes it among the most popular kinds of life insurance

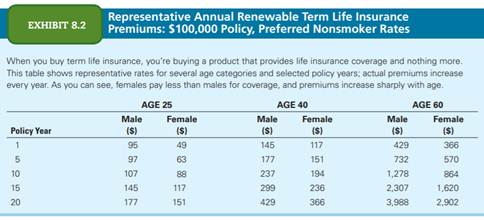

A 30-year-old man with a similar profile can expect to pay $29 monthly for the very same protection. AgeGender$250,000 coverage amount$500,000 protection quantity$1 million protection amount20Female$15$23$34Male$19$29$4830Female$15$23$37Male$18$29$4940Female$22$35$61Male$25$43$7550Female$44$78$139Male$57$102$18860Female$108$194$355Male$149$268$500 Collapse table Approach: Ordinary monthly prices are determined for male and female non-smokers in a Preferred health and wellness classification obtaining a 20-year $250,000, $500,000, or $1,000,000 term life insurance policy policy.

How do I get Level Term Life Insurance Policy Options?

Prices may vary by insurance company, term, protection amount, health and wellness course, and state. Not all plans are available in all states. Rate image valid since 09/01/2024. It's the most affordable type of life insurance policy for a lot of people. Degree term life is a lot extra affordable than a comparable whole life insurance policy. It's easy to handle.

It permits you to budget plan and plan for the future. You can easily factor your life insurance into your spending plan due to the fact that the premiums never ever change. You can prepare for the future simply as easily since you recognize exactly how much cash your liked ones will certainly get in the event of your absence.

Who are the cheapest Tax Benefits Of Level Term Life Insurance providers?

In these situations, you'll usually have to go with a new application process to get a far better price. If you still require coverage by the time your degree term life plan nears the expiry day, you have a few choices.

{kind=link}

Latest Posts

Instant Quote For Life Insurance

Final Expenses Benefit Old Mutual

End Of Life Insurance Coverage