All Categories

Featured

Table of Contents

Which one you pick relies on your demands and whether or not the insurer will accept it. Plans can also last up until defined ages, which for the most part are 65. Due to the various terms it provides, level life insurance policy offers possible policyholders with adaptable options. However yet surface-level info, having a higher understanding of what these strategies entail will help ensure you purchase a plan that meets your needs.

Be conscious that the term you pick will certainly affect the costs you pay for the plan. A 10-year degree term life insurance policy will set you back less than a 30-year policy since there's less opportunity of an occurrence while the plan is energetic. Reduced threat for the insurer relates to lower costs for the insurance policy holder.

Your family's age should likewise affect your plan term choice. If you have children, a longer term makes sense due to the fact that it shields them for a longer time. However, if your kids are near the adult years and will certainly be financially independent in the future, a shorter term may be a far better fit for you than a prolonged one.

Nonetheless, when contrasting entire life insurance policy vs. term life insurance, it's worth keeping in mind that the last commonly costs much less than the previous. The result is more protection with reduced costs, giving the finest of both worlds if you need a significant amount of protection yet can not manage a more expensive plan.

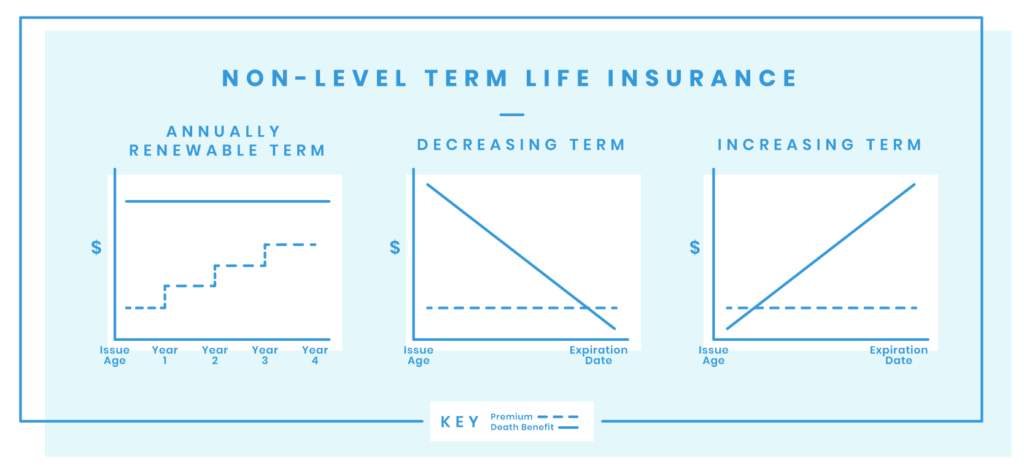

Is Annual Renewable Term Life Insurance Right for You?

A degree survivor benefit for a term plan usually pays as a lump sum. When that happens, your beneficiaries will obtain the whole quantity in a single payment, which amount is ruled out earnings by the internal revenue service. Therefore, those life insurance policy profits aren't taxed. Nonetheless, some level term life insurance policy business allow fixed-period repayments.

Rate of interest repayments received from life insurance policy plans are considered revenue and are subject to taxation. When your level term life policy runs out, a few different points can take place.

The disadvantage is that your renewable degree term life insurance will certainly include higher premiums after its initial expiry. Advertisements by Money. We might be made up if you click this advertisement. Advertisement For newbies, life insurance can be made complex and you'll have concerns you desire addressed prior to committing to any plan.

Life insurance policy companies have a formula for determining risk making use of death and passion (Simplified term life insurance). Insurance firms have hundreds of customers obtaining term life plans at the same time and make use of the costs from its active plans to pay surviving recipients of other policies. These business use mortality to approximate just how many people within a specific group will file death insurance claims each year, and that information is utilized to determine typical life span for potential policyholders

Furthermore, insurer can spend the cash they receive from premiums and increase their income. Because a level term policy does not have cash worth, as an insurance holder, you can not spend these funds and they do not offer retirement income for you as they can with whole life insurance coverage plans. The insurance company can spend the cash and make returns.

The list below area information the advantages and disadvantages of degree term life insurance policy. Predictable premiums and life insurance protection Simplified policy structure Prospective for conversion to irreversible life insurance policy Restricted coverage period No money worth accumulation Life insurance costs can boost after the term You'll discover clear advantages when comparing degree term life insurance policy to other insurance coverage types.

Understanding Level Premium Term Life Insurance

You always recognize what to anticipate with low-cost level term life insurance coverage. From the minute you get a plan, your costs will certainly never ever change, assisting you prepare financially. Your protection won't differ either, making these plans reliable for estate planning. If you value predictability of your payments and the payouts your heirs will certainly get, this kind of insurance might be an excellent suitable for you.

If you go this course, your premiums will boost but it's always excellent to have some versatility if you want to keep an energetic life insurance policy plan. Sustainable degree term life insurance is another choice worth considering. These policies enable you to keep your present plan after expiry, giving versatility in the future.

Why Short Term Life Insurance Could Be the Best Option?

Unlike a entire life insurance policy policy, degree term protection does not last forever. You'll pick a coverage term with the very best level term life insurance coverage rates, but you'll no longer have protection once the plan expires. This disadvantage can leave you rushing to discover a brand-new life insurance policy in your later years, or paying a premium to expand your existing one.

Lots of entire, global and variable life insurance policy policies have a cash worth component. With one of those policies, the insurance firm deposits a section of your regular monthly premium payments right into a cash value account. This account earns rate of interest or is spent, assisting it grow and offer an extra substantial payment for your recipients.

With a degree term life insurance policy, this is not the situation as there is no cash money value component. Because of this, your plan won't expand, and your survivor benefit will never enhance, consequently limiting the payout your recipients will receive. If you desire a policy that offers a survivor benefit and builds cash worth, explore entire, universal or variable plans.

The second your plan runs out, you'll no longer have life insurance policy protection. Level term and decreasing life insurance policy offer comparable plans, with the major difference being the fatality advantage.

It's a sort of cover you have for a certain quantity of time, called term life insurance policy. If you were to pass away while you're covered for (the term), your liked ones receive a set payout agreed when you secure the plan. You just select the term and the cover amount which you could base, for example, on the cost of elevating youngsters till they leave home and you could make use of the settlement towards: Helping to repay your mortgage, debts, credit history cards or loans Helping to pay for your funeral prices Helping to pay college charges or wedding costs for your kids Aiding to pay living expenses, replacing your income.

What is Life Insurance Level Term? Discover the Facts?

The policy has no cash value so if your repayments quit, so does your cover. The payment remains the very same throughout the term. If you take out a level term life insurance coverage policy you can: Choose a taken care of amount of 250,000 over a 25-year term. If during this moment you pass away, the payment of 250,000 will certainly be made.

{kind=link}

Latest Posts

Instant Quote For Life Insurance

Final Expenses Benefit Old Mutual

End Of Life Insurance Coverage