All Categories

Featured

Table of Contents

Rate of interest in solitary costs life insurance coverage is largely due to the tax-deferred treatment of the build-up of its cash money worths. Taxes will certainly be sustained on the gain, nonetheless, when you give up the policy.

The benefit is that enhancements in rate of interest will certainly be mirrored extra quickly in interest sensitive insurance than in typical; the negative aspect, certainly, is that lowers in interest prices will also be felt quicker in passion delicate entire life. There are 4 fundamental rate of interest sensitive entire life plans: The universal life policy is really greater than interest sensitive as it is developed to mirror the insurer's current death and cost as well as passion profits rather than historic rates.

What is the Role of Annual Renewable Term Life Insurance?

The company debts your premiums to the cash money value account. Regularly the company deducts from the money value account its expenses and the expense of insurance policy defense, usually defined as the death reduction charge.

Present assumptions are important to interest delicate items such as Universal Life. Universal life is likewise the most versatile of all the numerous kinds of policies.

The policy usually provides you a choice to pick one or 2 types of fatality benefits - Level term life insurance. Under one option your recipients obtained only the face amount of the policy, under the various other they get both the face amount and the cash worth account. If you desire the optimum quantity of survivor benefit currently, the 2nd option should be selected

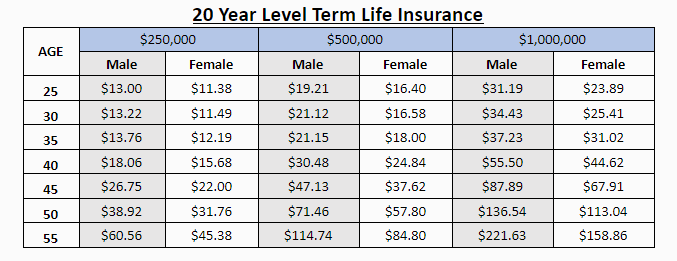

Why You Need to Understand 20-year Level Term Life Insurance

It is essential that these presumptions be reasonable since if they are not, you might need to pay more to keep the policy from lowering or lapsing. On the other hand, if your experience is much better then the assumptions, than you may be able in the future to miss a costs, to pay much less, or to have the plan paid up at a very early date.

On the various other hand, if you pay even more, and your assumptions are realistic, it is possible to compensate the plan at a very early date. If you surrender an universal life plan you might receive less than the money worth account due to surrender fees which can be of 2 types.

A back-end kind plan would certainly be more suitable if you plan to maintain protection, and the fee reduces with annually you continue the plan. Keep in mind that the rate of interest and expenditure and death costs payables initially are not ensured for the life of the plan. Although this kind of policy offers you maximum flexibility, you will require to proactively take care of the policy to maintain adequate funding, specifically due to the fact that the insurance policy firm can enhance death and expense charges.

You may be asked to make added premium payments where insurance coverage might terminate since the rates of interest dropped. Your beginning interest rate is fixed just for a year or in some cases three to 5 years. The ensured price supplied for in the plan is much reduced (e.g., 4%). Another attribute that is sometimes highlighted is the "no charge" financing.

You should get a certificate of insurance describing the arrangements of the group policy and any kind of insurance coverage fee. Normally the maximum amount of coverage is $220,000 for a home loan and $55,000 for all other financial debts. Credit life insurance policy need not be bought from the company granting the finance.

If life insurance is called for by a lender as a condition for making a finance, you might have the ability to appoint an existing life insurance policy plan, if you have one. However, you may desire to get team credit history life insurance coverage even with its higher cost as a result of its comfort and its availability, usually without thorough proof of insurability.

What Exactly is Guaranteed Level Term Life Insurance?

However, home collections are not made and premiums are sent by mail by you to the representative or to the business. There are particular elements that tend to raise the costs of debit insurance coverage greater than routine life insurance policy plans: Certain expenses coincide no issue what the size of the policy, to make sure that smaller plans provided as debit insurance policy will have greater premiums per $1,000 of insurance coverage than larger size normal insurance plans.

Because early gaps are costly to a company, the prices need to be handed down to all debit policyholders (Annual renewable term life insurance). Considering that debit insurance coverage is created to consist of home collections, higher payments and costs are paid on debit insurance policy than on regular insurance policy. In most cases these greater expenses are handed down to the policyholder

Where a business has different costs for debit and regular insurance coverage it might be possible for you to buy a larger amount of normal insurance than debit at no added price. If you are thinking of debit insurance, you should definitely investigate regular life insurance as a cost-saving choice.

This plan is developed for those that can not originally pay for the regular whole life premium but who desire the higher costs coverage and feel they will eventually be able to pay the greater costs. The family policy is a combination strategy that gives insurance security under one agreement to all participants of your prompt family hubby, better half and children.

Joint Life and Survivor Insurance offers coverage for two or more individuals with the fatality benefit payable at the death of the last of the insureds. Premiums are considerably lower under joint life and survivor insurance coverage than for plans that guarantee just one individual, given that the probability of needing to pay a fatality insurance claim is reduced.

All About What Does Level Term Life Insurance Mean Coverage

Costs are considerably higher than for plans that guarantee a single person, because the probability of having to pay a fatality case is greater. Endowment insurance provides for the payment of the face amount to your beneficiary if death happens within a particular time period such as twenty years, or, if at the end of the details period you are still alive, for the settlement of the face quantity to you.

Adolescent insurance policy provides a minimum of security and could supply coverage, which might not be available at a later date. Amounts supplied under such coverage are generally minimal based upon the age of the youngster. The present restrictions for minors under the age of 14.5 would certainly be the greater of $50,000 or 50% of the quantity of life insurance policy active upon the life of the applicant.

Adolescent insurance might be sold with a payor benefit motorcyclist, which offers forgoing future premiums on the kid's plan in the event of the fatality of the person that pays the costs. Elderly life insurance coverage, often referred to as graded fatality benefit plans, gives eligible older candidates with very little whole life protection without a medical checkup.

{kind=link}

Latest Posts

Instant Quote For Life Insurance

Final Expenses Benefit Old Mutual

End Of Life Insurance Coverage